Welcome to our comprehensive guide on the “Solution of Money and Credit of Class 10.” If you’re a Class 10 student seeking a deeper understanding of the intriguing world of money, credit, and financial systems, you’ve come to the right place. In this article, we present a well-structured and detailed solution to the chapter “Money and Credit” from the Class 10 curriculum.

Explore the various concepts and mechanisms related to money. Its role in an economy, the functioning of banks, and the significance of credit systems. With our expertly crafted explanations and step-by-step solutions, you’ll grasp the fundamentals and complexities of the financial world with ease. Let’s dive in and unlock the secrets of “Money and Credit of Class 10.

The fascinating chapter on “Money and Its Evolution” has been thoughtfully included in the Class 10 Economics curriculum. This chapter delves into the intriguing history of money, exploring its various forms and usage throughout different periods. Additionally, students will gain valuable insights into the interconnection between modern forms of money and the intricate banking system. As a comprehensive resource, this chapter concludes with exercise questions to test and reinforce students’ understanding of the subject matter. Prepare to embark on an enlightening journey through the evolution of money and its profound impact on economies worldwide.

Solution of NCERT Chapter 3 Economics Money and Credit of Class 10

Money and Credit of Class 10 Question and Solutions

Q 1. In situations with high risks, credit might create further problems for the borrower. Explain.

In situations with high risks, credit can indeed create further problems for the borrower. When a borrower takes on credit in a high-risk scenario, several potential issues may arise:

1. Increased Debt Burden: If the borrower faces difficulties in repaying the borrowed amount due to the high-risk nature of the venture, it could lead to an increased debt burden. This may result in mounting interest payments and the risk of defaulting on the loan, leading to further financial distress.

2. Financial Stress: High-risk situations are often associated with uncertain outcomes, such as in speculative investments or ventures with an uncertain future. If the borrower’s investment or venture does not yield expected returns, they may struggle to meet their credit obligations, leading to financial stress and potential insolvency.

3. Limited Access to Credit: High-risk borrowers may find it challenging to access credit in the future, especially if they have a history of defaulting on loans. Lenders may view them as risky borrowers and be hesitant to extend credit. It make difficult for them to meet their financial needs in the future.

4. Higher Interest Rates: Lenders typically charge higher interest rates to compensate for the increased risk they take when lending to high-risk borrowers. The higher interest rates can further strain the borrower’s financial situation, making it more challenging to repay the loan.

5. Adverse Impact on Credit Score: Failure to repay credit in a high-risk situation can adversely affect the borrower’s credit score. A poor credit score can hinder their ability to access credit in the future and may lead to limited financial opportunities.

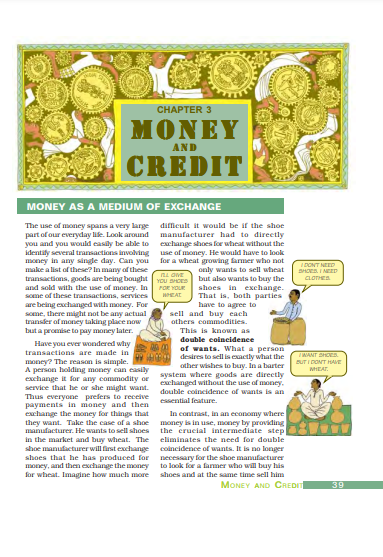

Q 2. How does money solve the problem of double coincidence of wants? Explain with an example of your own.

Money solves the problem of double coincidence of wants by acting as a medium of exchange. In a barter system, where goods and services are directly exchanged for other goods and services, there is a requirement for a perfect match of wants between two parties involved in the exchange. However, this can be challenging and inefficient, as finding someone who has what you need and needs what you have can be quite difficult.

With the introduction of money, individuals no longer need to find a direct coincidence of wants. They can exchange their goods and services for money, which is universally accepted as a medium of exchange. Money acts as an intermediary, enabling transactions to occur smoothly and efficiently.

For example, let’s consider a scenario in a barter system where Alice, who is a baker, needs a pair of shoes, and Bob, who is a cobbler, needs bread. In a barter system, Alice and Bob would have to find each other and directly exchange bread for shoes. However, this may not always be possible, and they may not come across each other at the right time.

Now, let’s introduce money into the scenario. Instead of directly exchanging bread for shoes, Alice and Bob can use money as an intermediary. Alice sells her bread to a customer for money, and Bob sells his shoes to the same customer for money. Then, Alice can use the money she earned to purchase the shoes from Bob. In this way, money facilitates the exchange between Alice and Bob, even though they do not have a direct coincidence of wants.

By eliminating the need for a double coincidence of wants, money greatly simplifies and accelerates economic transactions, making the exchange of goods and services much more efficient and convenient for everyone involved.

Q 3. How do banks mediate between those who have surplus money and those who need money?

Banks play a crucial role in mediating between those who have surplus money and those who need money. They act as financial intermediaries, facilitating the flow of funds between savers (those with surplus money) and borrowers (those in need of money). Here’s how banks perform this important function:

- Deposits and Savings: Individuals and businesses with surplus money deposit their funds in banks. These deposits can be in the form of savings accounts, fixed deposits, or other types of accounts. By depositing their money in banks, savers earn interest on their deposits, which encourages them to save and invest.

- Loan and Credit Facilities: On the other hand, banks offer various loan and credit facilities to individuals, businesses, and other borrowers who need money for various purposes, such as starting a business, buying a home, or financing their education. When borrowers take loans from banks, they agree to pay back the principal amount along with interest over a specific period.

- Intermediation: Banks act as intermediaries by using the deposits they receive from savers to extend loans and credit to borrowers. They channel funds from the surplus units (savers) to the deficit units (borrowers), effectively allocating capital to where it is needed most. This process ensures that the money is put to productive use and contributes to economic growth and development.

Overall, banks act as crucial financial intermediaries in the economy, bringing together those who have surplus money and those who need money, thereby supporting economic activities and promoting growth and development.

Q 4. Look at a 10 rupee note. What is written on top? Can you explain this statement?

At the top of a 10 rupee note, you will find the inscriptions “Reserve Bank of India” and “Guaranteed by the Central Government.” These statements hold significant importance as they indicate the authority and credibility behind the currency in India.

The Reserve Bank of India (RBI) serves as the central bank of the country and is responsible for issuing and regulating the currency. As the central banking institution, the RBI plays a crucial role in formulating monetary policies, managing the money supply, and maintaining the stability of the Indian rupee.

The statement “Guaranteed by the Central Government” signifies that the currency note is backed by the full faith and credit of the Indian government. This guarantee ensures the trust and confidence of the public in the value and acceptability of the currency for transactions within the country.

Both the Reserve Bank of India and the Central Government are the sole authorities responsible for issuing and managing currency in India. By inscribing these statements on the currency note, it is established that the note is officially authorized, and its value is supported by the combined authority of the central bank and the government.

This ensures the smooth functioning of the monetary system, instills public confidence in the currency’s stability, and upholds the integrity of the Indian rupee as a reliable medium of exchange for economic transactions.

Q 5. Why do we need to expand formal sources of credit in India?

Expanding formal sources of credit in India is essential for several reasons:

1. Financial Inclusion: Expanding formal credit sources ensures that a larger section of the population, including the unbanked and financially marginalized, has access to financial services. This promotes financial inclusion and empowers individuals and businesses with opportunities to participate in the formal economy.

2. Reduced Dependence on Informal Credit: In India, a significant portion of the population relies on informal sources of credit, such as moneylenders and local lenders, which often charge high-interest rates. By expanding formal credit channels, people can access credit at more reasonable and regulated interest rates, reducing their dependency on exploitative informal sources.

3. Boost to Economic Growth: Adequate and accessible credit facilities fuel economic growth by promoting investments, entrepreneurship, and business expansion. Formal credit institutions can cater to the financial needs of small and medium-sized enterprises, which play a crucial role in driving economic development.

4. Employment Generation: When businesses have access to formal credit, they can expand their operations, invest in technology, and create more job opportunities. This, in turn, leads to improved livelihoods and increased economic activity.

5. Financial Stability: Formal credit institutions are regulated and supervised by the central bank. It ensures prudent lending practices and risk management. This contributes to financial stability and reduces the likelihood of systemic risks in the economy.

By expanding formal sources of credit, India can achieve broader financial inclusion, sustainable economic growth, and equitable development, benefitting individuals, businesses, and the nation as a whole.

Q 6. What is the basic idea behind the SHGs for the poor? Explain in your own words.

The basic idea behind Self-Help Groups (SHGs) for the poor is to empower marginalized individuals, particularly women, by bringing them together to form a collective and supportive platform. SHGs are small voluntary associations formed at the community level, comprising members from similar socio-economic backgrounds.

The primary objective of SHGs is to promote financial inclusion, social cohesion, and economic empowerment among its members. Members contribute small amounts of savings regularly to create a common fund. This fund is then utilized to provide microcredit and loans to the group members for various income-generating activities and personal needs.

SHGs enable the poor to access financial services, build a savings habit, and access credit without relying on traditional banks or moneylenders. By pooling their resources, SHG members can collectively address their financial requirements and uplift their socio-economic status.

Moreover, SHGs also serve as platforms for capacity building, skill development, and knowledge-sharing among members. They encourage leadership, decision-making, and entrepreneurship skills, fostering a sense of ownership and responsibility among the participants.

Furthermore, SHGs promote social solidarity and support systems among the members. They create a sense of belonging and encourage mutual trust and cooperation. Members share their experiences, offer emotional support, and collectively address various social and economic challenges faced by their community.

In summary, SHGs for the poor aim to promote self-reliance, financial independence, and socio-economic empowerment among marginalized individuals by providing them with access to credit, financial literacy, and a supportive community. Through these groups, the poor can break the cycle of poverty, improve their livelihoods, and lead a dignified life.

Q 7. What are the reasons why banks might not be willing to lend to certain borrowers?

Banks might not be willing to lend to certain borrowers due to various reasons, including:

1. Poor Credit History: If a borrower has a history of defaulting on previous loans or has a low credit score, banks may consider them as high-risk borrowers and may be reluctant to lend to them.

2. Insufficient Income: Banks assess a borrower’s ability to repay the loan. If the borrower’s income is not sufficient to cover the loan repayments, the bank may deny the loan application.

3. Lack of Collateral: Some loans, especially large ones, may require collateral as security. If a borrower does not have sufficient assets to offer as collateral, the bank may be hesitant to approve the loan.

4. Unstable Employment: Banks prefer borrowers with stable employment history as it indicates a steady source of income. Borrowers with irregular or uncertain employment may face difficulties in obtaining loans.

5. High Debt-to-Income Ratio: If a borrower already has significant existing debts in relation to their income, the bank may be concerned about their ability to manage additional loan repayments.

6. Industry Risk: Banks may avoid lending to borrowers in industries that are considered high-risk or volatile.

7. Lack of Documentation: Insufficient or incomplete documentation can lead to loan rejection as banks require proper verification of a borrower’s identity, income, and other relevant information.

8. Age of the Borrower: Some banks have age restrictions for borrowers, especially for long-term loans, as older borrowers may be perceived as having higher repayment risks.

It is important for borrowers to understand these factors and maintain a good financial profile to increase their chances of obtaining loans from banks and other financial institutions.

Q 8. In what ways does the Reserve Bank of India supervise the functioning of banks? Why is this necessary?

The Reserve Bank of India (RBI) supervises the functioning of banks in several ways to ensure financial stability and maintain the integrity of the banking system. It employs both on-site and off-site inspections to assess banks’ financial health, risk management practices, compliance with regulations, and governance standards.

RBI also sets prudential norms and guidelines for capital adequacy, asset quality, and liquidity to safeguard depositors’ interests and maintain the overall health of the banking sector.

This supervision is crucial to prevent risks, detect potential issues early on, and take corrective measures to protect the interests of depositors, maintain financial stability, and foster a sound and secure banking environment in the country.

Q 9. Analyse the role of credit for development.

Credit plays a vital role in driving economic development by providing financial resources to individuals, businesses, and governments. It fuels investment, fosters entrepreneurship, and promotes job creation, leading to increased productivity and overall growth.

Access to credit empowers the poor, promotes financial inclusion, and supports poverty alleviation efforts. Moreover, credit facilitates the development of critical infrastructure, technological advancements, and industrial growth.

However, proper supervision and regulation by institutions like the Reserve Bank of India are essential to prevent misuse and ensure financial stability. By balancing credit availability and risk management, economies can harness its potential to drive sustainable development and improve living standards.

Q 10. Manav needs a loan to set up a small business. On what basis will Manav decide whether to borrow from the bank or the moneylender? Discuss.

Manav’s decision to borrow from a bank or a moneylender will depend on several factors. If Manav can meet the bank’s eligibility criteria and has a good credit history, borrowing from the bank may offer several advantages. Banks generally provide loans at lower interest rates, flexible repayment terms, and are regulated by authorities, ensuring fair practices.

On the other hand, if Manav faces challenges in meeting the bank’s requirements or has a poor credit history, the moneylender might be more accessible. Moneylenders may offer quick loans without strict eligibility checks, but often charge higher interest rates.

Manav should carefully consider the terms, interest rates, and the reputation of the lender before making an informed decision to ensure financial stability and avoid potential debt traps.

Q 11 (a). Why might banks be unwilling to lend to small farmers?

Banks might be unwilling to lend to small farmers due to various reasons:

1. Lack of Collateral: Small farmers often lack substantial assets or collateral to secure loans, making banks hesitant to extend credit, as they face higher risks of default.

2. Uneven Income and Cash Flows: Agricultural income is seasonal and dependent on factors like weather and crop yield. Banks may perceive this income variability as a risk, leading to reluctance in lending.

3. Limited Financial Literacy: Some small farmers may have limited financial literacy and struggle with documentation and loan procedures Thus it is challenging for banks to assess their creditworthiness.

4. High Administrative Costs: Providing small loans to numerous farmers can result in high administrative costs for banks, making it less profitable for them.

5. Previous Loan Defaults: If small farmers have a history of loan defaults, banks may become cautious about lending to them in the future.

To address these challenges, governments and financial institutions can work on providing targeted support. Also, promoting financial literacy among farmers, and offering loan products tailored to their specific needs.

Q 11 (b). What are the other sources from which the small farmers can borrow?

Banks might be unwilling to lend to small farmers due to several reasons. Firstly, small farmers often lack proper collateral or credit history, making them riskier borrowers in the eyes of banks.

Additionally, the administrative costs associated with processing small loans may deter banks from lending to them. Moreover, unpredictable weather conditions and the vulnerability of agriculture as an economic activity can affect the repayment capacity of small farmers.

As a result, banks may prefer larger and more established borrowers with higher creditworthiness. To address this issue, the government and financial institutions need to implement measures to support and incentivize banks to provide affordable credit to small farmers, ensuring their financial inclusion and agricultural development.

Q 11 (c). Explain with an example of how the terms of credit can be unfavourable for the small farmer.

Let’s take the example of a small farmer named Ramesh who needs a loan to purchase seeds and fertilizers for the upcoming crop season. He approaches a local moneylender as he faces difficulty obtaining credit from a formal financial institution.

The moneylender agrees to lend Ramesh the required amount but imposes a high-interest rate of 24% per annum, significantly above the prevailing market rate. Additionally, the moneylender demands that Ramesh repay the loan within three months, leaving him with a short repayment period.

This unfavorable term puts immense financial pressure on Ramesh, making it challenging for him to repay the loan on time. Leading to a cycle of debt and financial vulnerability for the small farmer.

Q 11 (d). Suggest some ways by which small farmers can get cheap credit.

Small farmers face challenges in accessing credit from formal financial institutions due to various reasons. Banks may be unwilling to lend to small farmers because of their limited financial resources. Also due to lack of collateral, and higher credit risk associated with agriculture.

Small farmers often operate on small landholdings, making it difficult for banks to recover loans in case of default. Additionally, the seasonal and unpredictable nature of agriculture poses risks to loan repayment. As a result, banks may perceive lending to small farmers as less profitable and may prefer lending to more established and creditworthy borrowers.

To address this, governments and financial institutions must design tailored credit schemes and improve financial inclusion to support the needs of small farmers.

Q 12. Fill in the blanks:

- Majority of the credit needs of the _________________households are met from informal sources. (Answer: Poor)

- ___________________costs of borrowing increase the debt-burden. (Answer: High)

- __________________ issues currency notes on behalf of the Central Government. (Answer: Reserve Bank of India)

- Banks charge a higher interest rate on loans than what they offer on __________. (Answer: Deposits)

- _______________ is an asset that the borrower owns and uses as a guarantee until the loan is repaid to the lender. (Answer: Collateral)

Q 13. Choose the most appropriate answer.

1. In an SHG, most of the decisions regarding savings and loan activities are taken by

-

-

- Bank

- Members

- Non-government organisation

-

Answer: 2. Members

2. Formal sources of credit do not include

-

-

- Banks

- Cooperatives

- Employers

-

Answer: 3. Employers

Money and Credit of Class 10 Summery

“Money and Credit” is a crucial chapter in Class 10 Economics that explores the concepts of money, credit, and their significance in the economy. The chapter delves into the history of money, the evolution of different forms of money, and how modern forms of money are linked to the banking system.

It also highlights the role of banks in mediating between surplus money and those in need of credit. The chapter discusses the importance of formal sources of credit and the challenges faced by small farmers in accessing credit.

It further explains the functioning of Self-Help Groups (SHGs) for the poor and the need for expanding formal sources of credit in India. Overall, “Money and Credit” offers valuable insights into the functioning of the monetary and credit systems, providing students with a comprehensive understanding of these vital economic aspects.

Read Also:

Frequently Asked Questions – FAQs on Money and Credit Class 10

Q 1. Importance of money and credit for class 10 students?

The chapter on “Money and Credit” holds immense importance for Class 10 students. It provides a fundamental understanding of the crucial role of money and credit in an economy.

By studying this chapter, students grasp the concept of money as a medium of exchange, unit of account, and store of value. They learn about various forms of money used historically and the evolution of modern banking systems. Understanding credit becomes essential as it enables students to comprehend the financial needs of different sections of society, especially small farmers and the poor.

Overall, this chapter equips students with essential knowledge about the functioning of monetary systems. Also, about significance of credit in fostering economic development and financial inclusion.

Q 2. What are the various Sources of Credit for Rural Households?

Rural households in India have access to various sources of credit to meet their financial needs. Some of the significant sources of credit for rural households include:

1. Formal Financial Institutions: These include banks, cooperative societies, and regional rural banks. They offer agricultural loans and other financial services to farmers and rural households.

2. Self-Help Groups (SHGs): SHGs are community-based organizations. It provide micro-credit and other financial services to their members, primarily women, in rural areas.

3. Moneylenders: Despite the formal financial institutions, moneylenders still play a role in rural credit. Especially in remote areas where formal credit is not easily accessible.

4. Microfinance Institutions: Microfinance institutions offer small loans and financial services to low-income individuals, including rural households, to support their livelihood activities.

5. Government Schemes: Various government schemes provide credit support to rural households for agricultural and entrepreneurial activities. Also for promoting rural development and financial inclusion.

Rural households often rely on a combination of these sources to fulfill their credit requirements and improve their economic well-being.

Q 3. What are the various modern form of money?

- Cash

- Deposits in Bank

- Check